Meta: Confused abot SIP or LIC for 2025? Examine returns, risks, and long-term advantages in extensive depth to find a better investment path. Today, make wise financial selections.

When it comes to investing, Indian households sometimes have to decide between modern wealth-building techniques and traditional insurance plans.

In this field, two well-liked challengers are SIP (Systematic Investment Plan) and LIC (Life Insurance Corporation of India) products.

The financial aspirations, risk tolerance, and investing perspective of people are changing as we enter 2025. This makes the discussion of SIP against LIC more relevant than it has ever been.

Here, we will provide clarity on whether investing in 2025 is the wiser choice. We will examine the features of every investing tool, their advantages and drawbacks, and finally, which one fits more of today's financial objectives.

Understanding SIP vs. LIC will enable you to make a better investment decision that fits your long-term vision, regardless of your income level, family situation, or approaching retirement.

What is a SIP (Systematic Investment Plan)?

What is a SIP (Systematic Investment Plan)?

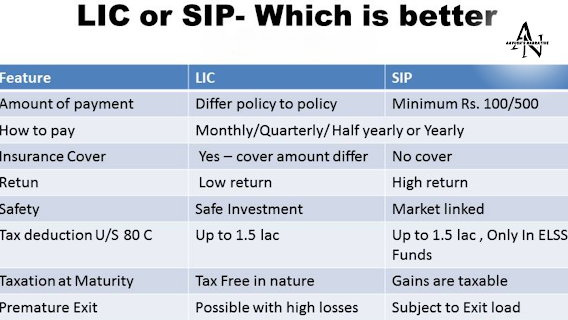

Usually, monthly or quarterly, a Systematic Investment Plan (SIP) is a technique for consistent mutual fund investment.

With compounding, SIP lets you start small and increase your investment over time instead of making a big sum payment.

Important SIP characteristics:

- Returns related to the markets include owning either debt or equity mutual funds.

- Start with ₹500 or more.

- Disciplined investing promotes consistent saving.

- Reducing the effect of market volatility, penny-cost averaging helps.

- High liquidity refers to any time (except for ELSS funds with a 3-year lock-in).

What is an LIC (Life Insurance Corporation) policy?

Licensed plans are conventional financial tools combining savings with life insurance. Among the several policies LIC provides are investments, whole life plans, term insurance, and ULIPs.

These obligations, which are usually long-term, seek to offer both a savings component and financial security.

Important features of LIC:

- The death benefit from life coverage falls to the nominees.

- Usually, most plans provide guaranteed maturity benefits.

- Policies could provide for annual or terminal bonuses.

- Section 80C allows premiums to be tax-deductible.

- Low risk: The Indian government backs LIC.

Risk and Return: Where Do You Earn More?

Risk and Return: Where Do You Earn More?

- SIP:

Linked to mutual funds investing in debt securities or stocks are SIPs. Although they expose market risks, historical evidence indicates that long-term SIPs typically yield better returns, often in the range of 10–15%.

- LIC:

Most LIC policies, especially endowment plans, offer assured but meager returns of 4–6%. Their first concern is capital preservation above income increases.

Results: SIPs provide superior returns and, therefore, are the wiser investment option for long-term wealth accumulation for goal-oriented investors in 2025.

Tax Benefits: SIP and LIC Both Offer Relief

While there is a small distinction, SIP and LIC both qualify for tax deductions.

SIP (ELSS)

- It is eligible under Section 80C up to ₹ 1.5 lakh/year.

- Three-year lock-in term.

- Returns are taxed at 10% after ₹1 lakh as LTCG, or long-term capital gains.

LIC:

- Section 80C lets premiums be deducted.

- Under Section 10(10D), maturity proceeds are tax-free, subject to restrictions.

Result: While LIC fits individuals who desire assured, tax-free profits, ELSS via SIP can be a wiser investment decision if you're searching for larger yields, together with tax benefits.

Risk Factor Comparison

SIP investments have a direct connection with the market. Though they have modest-to- great risk, they provide more return possibilities.

Because the government guarantees support for LIC policies, especially traditional ones, they are low-risk.

Therefore, LIC would look intriguing if you are a conservative investor. On the other hand, a deliberate risk in SIPs could be a wiser investing option for long-term wealth building.

Returns on Investment

Returns on Investment

Where SIPs shine over LIC, it returns.

- Historically, over a 10–15 year period, equity mutual funds have provided annualized returns of 12–15%.

- Traditional LIC policies may hardly match inflation with their yields of 4–6% post-bonus and loyalty enhancements.

Clearly, in the fight between SIP and LIC, SIP prevails in terms of returns, especially if you choose excellent mutual funds and remain invested long-term.

Liquidity and Flexibility

Liquidity and Flexibility

SIPs have more liquid qualities. Any time you halt, raise, lower, or pause your investments without penalties, you can. By contrast, LIC rules are inflexible. Early surrendering usually means a loss.,

In the uncertain environment of today, flexibility is essential and gives SIP still another benefit in the SIP vs. LIC debate.

Investment Horizon and Goals

- Short- to Mid-Term Goals (3-7 years): SIPs are perfect for travel, electronics, or housing down payments, especially.

Ten-plus years: SIPs support wealth building, children's education, and retirement

- LIC: Designed for people who give life cover top priority over returns.

SIP is without a doubt the better investing option if your focus is wealth above only protection.

SIP vs. LIC for Young Investors

SIP vs. LIC for Young Investors

By 2025, young professionals want financial flexibility and wealth growth above strict saving plans. SIP matches their way of life exactly:

- Little expenditures now have enormous future value.

- Compounder's power

- Lots of liquidity and adaptability

- Matches both long- and short-term objectives.

LIC could seem antiquated for young investors, particularly when seen only as an investment rather than protection.

SIP vs. LIC for Retirement Planning

Are you preparing for your retirement? Over 20 to 30 years, SIPs in balanced, index, or large-cap funds can offer a strong corpus. For tax advantages, include an ELSS.

Though low-risk, LIC might not grow an adequate corpus given low returns.

Therefore, SIP becomes a better investment option for a safe and financially independent retirement.

Which is the smarter investment choice for 2025?

Which is the smarter investment choice for 2025?

Let's call the discussion over here.

- Are you interested in wealth creation? SIP won.

- Ask for insurance using savings. Think about LIC.

- Want long-term growth, more returns, and flexibility? SIP, once more, is your friend.

The concept is to know where SIP and LIC fit in your financial plan rather than to set them against each other as rivals.

Invest in SIPs for growth and choose a pure term insurance plan (less expensive than investment-based policies) for lifetime coverage. Often the wiser investing option for 2025 and beyond is this combo.

Conclusion

It's not difficult to decide which of SIP or LIC to use. Investments must be wiser in 2025 with inflation, growing costs, and the requirement of financial freedom.

SIPs meet all the necessary criteria due to their superior yields, flexibility, and tax-saving options.

Although still valuable, life insurance primarily serves as a form of protection. Combining SIPs with term insurance instead of LIC's packaged products will probably result in a wiser investment decision fit for the financial situation of today.

Clearly state your objectives, understand your risk tolerance, and carefully diversify. This is because there is no one-size-fits-all approach to investing, but rather, one must make wise decisions.

Frequently Asked Questions (FAQs)

Frequently Asked Questions (FAQs)

1. For long-term investing, is SIP better than LIC?

Yes, over the long run, SIPs usually provide more returns than conventional LIC policies. For the generation of money, they are superior.

2. Can I fund both SIP and LIC?

Of course. While LIC offers life cover, SIPs will enable you to increase your wealth. Just be certain your objectives match your investments.

3. Which is safer: SIP or LIC?

In terms of assured returns, LIC is safer; SIPs, however, are market-linked and provide more potential over time.

4. Does SIP provide insurance like LIC?

No, SIP excludes life insurance. More reasonably priced is a separate term plan for life cover.

5. Which of the two investments, SIP or LIC, is better for 2025?

Because of their flexibility, greater returns, and fit for long-term objectives, SIPs are considered the smarter investing option for 2025.

{kind=link}

0 Comments